January 09, 2003

Theory of the Firm

The point of this lecture is to show that the supply curve is the marginal cost curve under the assumptions of profit maximizing behavior and a price taker.

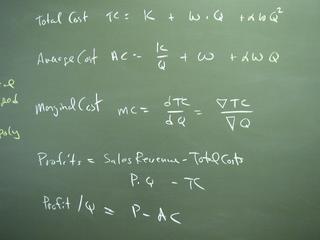

The theory of the firm is based on production technology. Q = f(K,L). We will assume that K is fixed in the short run. Changing L and, hence, Q changes the firm's cost of production.

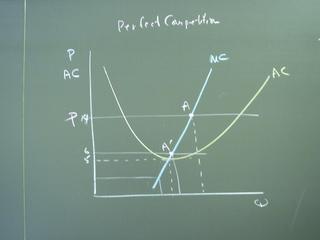

Here is a firm with a profit maximizing position A for a price of 14 and a profit maximizing position A' for a price of 6. Notice that the firm does not produce at the minimum average cost position.

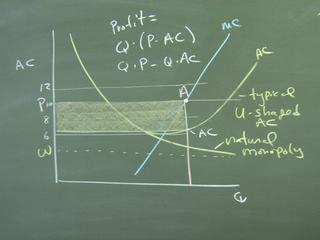

Another version of this diagram shows the profits as a shaded rectangle. Producing at A produces the rectangle with the largest area. (The area is quantity times price - quantity times average cost.) Producing at the point of minimum average cost would produce the tallest rectangle, but you give up too much on length compared to A.

We also see here the AC curve for a natural monopoly. (This was the algebra without the Q-squared terms.)

A proof that the MC curve goes through the AC curve at its minimum, where it is flat:

This also demonstrates why the MC curve is above (below) the AC curve when the AC curve is increasing (decreasing).

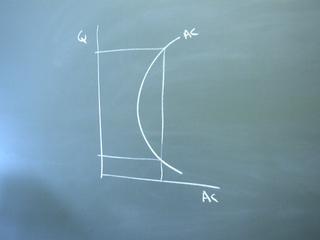

The horizontal axis in supply and demand is Q because otherwise we would have to do the theory of the firm like this. A U-shaped AC curve is a function. A C-shaped AC curve is not a function.

See also: http://www.econmodel.com/classic/ucost1.htm