January 30, 2003

Mortgages and Interest Rate Changes

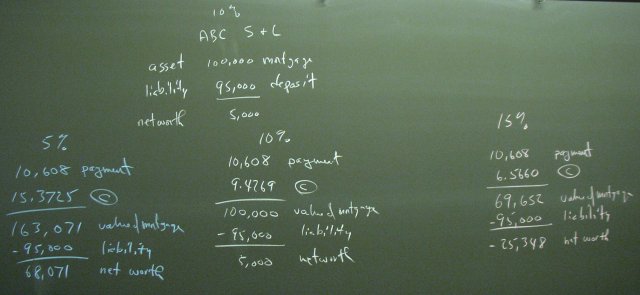

A bank makes a 10% 30-year fixed rate mortgage for $100,000 using $95,000 of deposits and $5,000 of their own money. When interest rates go up, the value of the mortgage in the secondary market plummets, and the bank is insolvent. Normally, the government would shut down the bank and pay off the insured depositors. Banks do not like higher interest rates.

When interest rates decrease, the value of the mortage would soar except for one important point. People have the right to pay off mortgages early. The balance due is the present value of the remaining payments at the original interest rate. Purchasers of mortgages in the secondary market are aware that they might be about to get a check for $100,000 as payment in full on a mortgage even though the present value of the remaining payments is $163,071. Therefore, the mortgage will never be worth more than about $110,000 in the secondary market. Banks are not really happy about lower interest rates either. Banks like stable interest rates.

Why do people invest in mortgages in the first place? They do so because the return is typically a little higher than it is on noncallable government bonds. Corporate bonds often have a call option allows the borrower to pay the bond off early at something close to the face value. The return on corporate bonds is a little higher than the return on noncallable bonds to compensate the investor for taking the risk that the call option might be exercised.

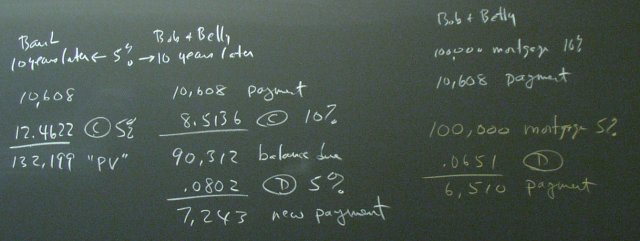

We concluded with a stirring discussion of how Bob and Betty might do the refinance calculations 10 years after they took out the loan.